Professionals who have experience with anti-money laundering laws are not shocked by the indictment of the Southern Poverty Law Center (SPLC). If the facts alleged in the indictment are true, they appear to support charges that are unremarkable and to be expected. Those allegations also strongly suggest the possibility of more indictments.

That reaction isn’t the loudest response, right now. Indicted for fraud, making false statements to a bank, and conspiracy to commit money laundering, the SPLC is hinting broadly at a victimhood defense about being a left-wing organization politically targeted by a right-wing administration. Among the army of lawyers the SPLC has hired from multiple law firms, the racial justice nonprofit is now represented by the D.C. insider Abbe Lowell, who also represented Hunter Biden. Reuters describes Lowell’s boutique law firm as one that works “defending Trump targets.”

Spreading the victimhood narrative, journalists in legacy media are suggesting that the prosecution is a faked-up political hit built on shaky legal ground; MS Now calls the charges “nakedly political.” Joining that chorus, Chicago Tribune columnist Clarence Page reads undertones of menace in an indictment that he describes as “murky.”

It’s not murky. You can read the indictment here. Among other things, the SPLC is accused of creating accounts at two banks for fake businesses that “were never incorporated, had no bona fide employees, and conducted no actual business.”

That’s hard to do. The Bank Secrecy Act of 1970, updated after 9/11, creates extensive anti-money laundering “know your customer” rules that require banks to identify new customers and be sure a business is both real and representing its activities in an honest way. You can read the regulatory requirement for a “customer identification program” yourself, and look at bank websites to see what kinds of documents you have to show a bank to open a new business account: articles of incorporation, tax forms, permits, personal identification to show who is opening the account, and so on.

Kevin Sullivan is a retired New York State Police detective who served on multijurisdictional fraud task force investigations, and is also the author of an anti-money laundering (AML) guidebook for businesses. In retirement from law enforcement, he’s the president of an AML training academy. An investigation into allegedly fake bank accounts, he told The Federalist, has to start with a basic question: “How the heck did these businesses obtain an account in the first place?”

Well before anyone could begin using bank accounts in questionable ways, Sullivan said, “warning signs should have appeared at the account opening due diligence phase. Prospective banking customers that lacked appropriate verifying information, such as, never incorporated, no bona fide employees and no actual business, should never have been accepted as a customer by any financial institution.”

One of a short list of things has to have happened, the Texas A&M law professor and AML scholar William Byrnes told The Federalist, if the SPLC opened bank accounts for businesses that didn’t exist: banks ignored their legal obligations and opened accounts without knowing their customers, banks had insiders who sneaked around the requirement because of a relationship with the people opening the fake accounts, or the people opening the fake accounts showed the bank forged business documents.

“If the allegation is correct,” Byrnes told The Federalist, “then it’s one of those three.”

Speaking to those possibilities, the indictment specifically alleges that the bank accounts were associated with fake documents delivered by SPLC employees: “Employee-1, and others, signed these documents containing false and misleading statements for the benefit of the SPLC.”

In any case, the documents that were allegedly used to open the accounts would be retained by the banks. Regulators routinely visit banks to check on their compliance with “know your customer” laws, Byrnes says, and to evaluate a bank’s recordkeeping on customers. Whatever paperwork the bank had when they opened the SPLC’s allegedly fake business accounts would still be on hand for federal prosecutors to use in court.

This is one of the other shoes that might still drop. Asked if the paperwork retained by the bank would identify the individual who allegedly opened the accounts on behalf of the SPLC, Byrnes didn’t hesitate: “One hundred percent. Absolutely.” If prosecutors have accurately described the activity alleged in the indictment, those individuals also face the distinct possibility of being personally indicted. “Because some human being faked the documents,” Byrnes said, and opening a bank account for a fake business using fraudulent documents is a crime, or possibly several.

The “know your customer” expectation goes deeper: A bank is expected to know its customers, but also to have some sense of the customer’s customers and business. A business account should have a history of transactions that look like the kind of transactions that the type of business would be expected to do. As an example, a business identifying itself to its bank as a single small convenience store probably shouldn’t execute a bunch of seven-figure transactions. The cash flow at a small photography studio should look like the cash flow at a small photography studio.

“Electronically, every bank has at least some minimum software that looks for these anomalies,” Byrnes said, and transactions that don’t make sense can trigger a suspicious activity report to the federal Financial Crimes Enforcement Network (FinCen) – a bureau of the Department of the Treasury. FinCen evaluates suspicious activity reports, then passes on significant reports to regulators and law enforcement agencies.

The SPLC allegedly opened bank accounts for fake businesses that didn’t do the type of work those businesses were supposed to be doing: a supposed photography studio that just made payments to informants, a rare books warehouse that just made payments to informants, and so on. Those are the kinds of anomalous transactions that tend to trigger suspicious activity reports, which can end up in front of law enforcement agencies.

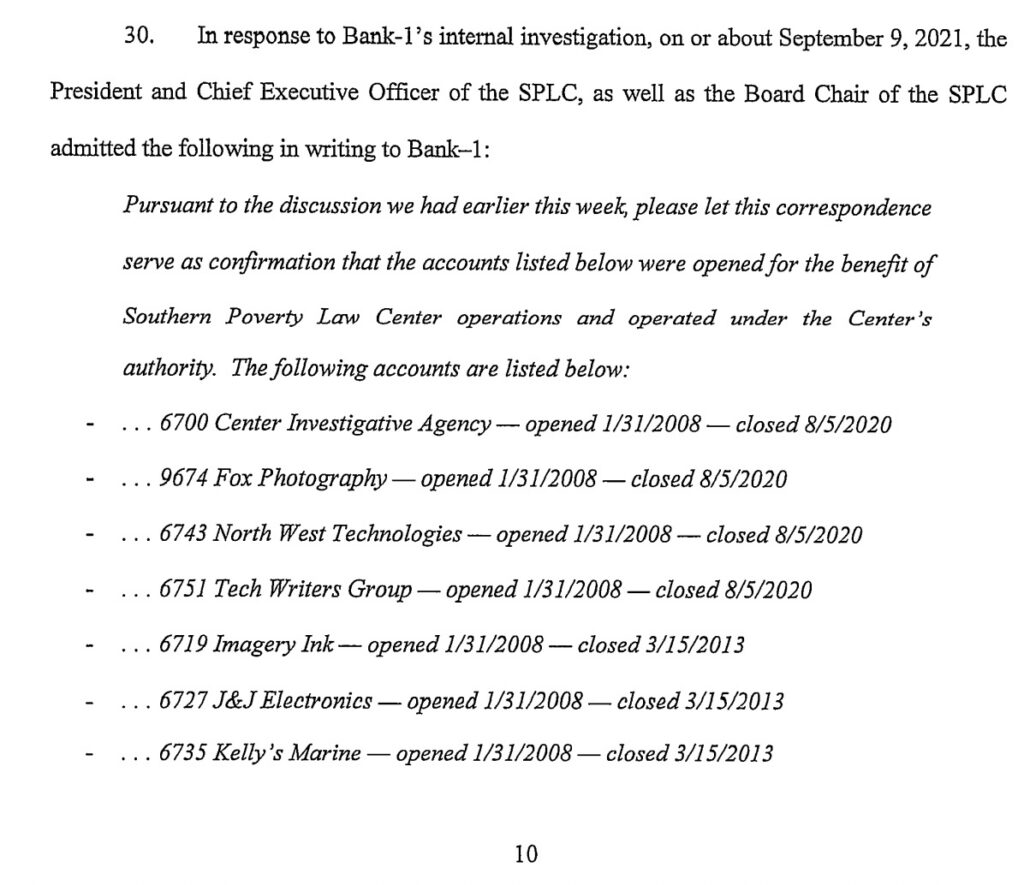

If the indictment is accurate, it contains an astonishing detail. Here’s a screenshot so you can see it straight from the document:

If the indictment correctly describes these letters, then the SPLC admitted to a bank, in writing, to opening accounts for businesses that didn’t exist. “That’s certainly an admission of fraud against the bank,” Byrnes told The Federalist. Remember that a Chicago Tribune columnist is calling the indictment “murky,” and read the government’s description of the SPLC’s letter to its bank again.

Once you begin pulling at the threads suggested by the indictment, a long list of other questions comes up pretty quickly. If the SPLC made payments to informants through fake shell companies, were the payments reported to the IRS with 1099s? Did the recipients pay taxes on the payments? What are the legal implications when a non-profit corporation makes payments to people through shell entities that are not registered as non-profit corporations? There are a considerable number of avenues for further investigation.

Byrnes shrugs at the claims of a politicized prosecution. “Fraud is fraud,” he said. If the SPLC used fraudulent documents to lie to banks and obtain accounts for businesses that didn’t exist, they will have created a substantial paper trail as evidence of crimes that are not obscure or rarely noticed. Maybe another administration wouldn’t have chosen to pursue the case, he said, but “that doesn’t mean that the crimes aren’t being committed.”

In court, the SPLC was first represented by William Athanas, a lawyer specializing in white collar crime who divides his practice between Birmingham and the District of Columbia. By email, the Federalist asked Athanas a series of questions about his client, starting with this one: “Does the SPLC agree that it opened bank accounts for fictitious businesses that ‘were never incorporated, had no bona fide employees, and conducted no actual business,’ or does the SPLC dispute that claim?” Athanas did not respond before publication time.