Many Republicans have spent the last four-and-a-half years crowing about how they will “repeal and replace” Obamacare, believing it to be anathema to the Constitution, the American way of life, and human liberty itself. A number of politicians and candidates also seem to believe that vowing to repeal and replace the federal health care law was and is necessary to survive primary challenges, win elections, or position themselves for future campaigns.

All of that is fine, as far as it goes. But it is not very helpful from a policy standpoint, in part because it implies that Obamacare upended a long and fine tradition of free-market healthcare in our country that was humming along perfectly well until President Obama and Congressional Democrats came along and changed everything, which simply isn’t true.

Plenty of Republican leaders know that, but the implication remains—not least because most Americans don’t know the troubled history of our health care system. The government takeover of healthcare didn’t happen in 2010, it happened in 1965 with the creation of Medicare and Medicaid. Some would argue it began even earlier, during World War II, when a federal court ruled that employer payments to health insurers did not count as taxable employee income, a ruling that was codified a decade later by the Internal Revenue Service, thus creating a huge incentive for employers to compensate their workers with tax-free health benefits. This is why employer-sponsored health insurance is now the single largest federal tax expenditure, by a large margin.

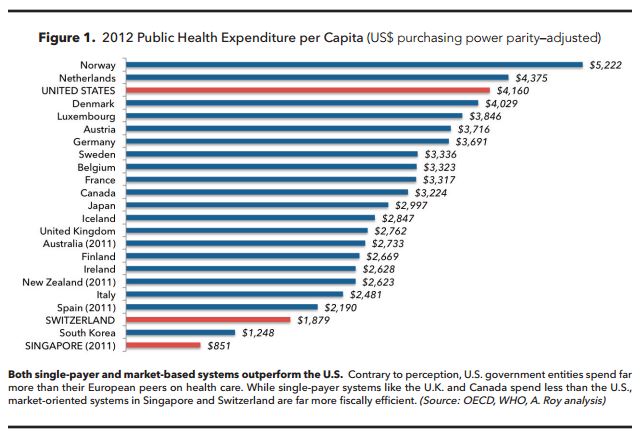

In the decades since, government spending on healthcare has grown exponentially, such that only two other countries spend more tax dollars on health care than the United States: Norway and the Netherlands. Overall per capita healthcare spending in the United States is of course the highest in the world by far, in excess of $8,200. There are many reasons for this: the tax exemption for employer-sponsored coverage, Medicare payment policies that favor hospital treatment, a Medicaid funding scheme that incentivizes states to always spend more, and so on.

In other words, getting rid of Obamacare will not solve our health care problems because our biggest problems predate the Affordable Care Act (ACA). Because the Republican emphasis tends to be on repeal rather than replace (our health care system is byzantine, after all, and it’s easier to be against something obviously flawed than to support something new and complicated), the message that often comes through is that GOP leaders don’t really care whether poor people have health insurance or not and the best thing we can do at this point is to shut the whole thing down—even if that means millions of Americans will lose their subsidized Obamacare coverage.

In other words, getting rid of Obamacare will not solve our health care problems because our biggest problems predate the Affordable Care Act (ACA). Because the Republican emphasis tends to be on repeal rather than replace (our health care system is byzantine, after all, and it’s easier to be against something obviously flawed than to support something new and complicated), the message that often comes through is that GOP leaders don’t really care whether poor people have health insurance or not and the best thing we can do at this point is to shut the whole thing down—even if that means millions of Americans will lose their subsidized Obamacare coverage.

Repeat: Conservatives Have Good Health Care Ideas

Of course, that’s not what Republican leaders think at all. In fact, since Obamacare’s passage Republicans have come forward with a number of thoughtful replacement plans that would not only roll back the law’s excesses but also address pre-ACA problems that had festered for too long. In light of all that’s happened since 2010, it’s a shame more of these Republican plans didn’t surface when the GOP was in a better position to pursue them.

The truth is, Obamacare didn’t create something new or innovative so much as radically double down on some of the worst aspects of existing health care policy—increasing government control over private health insurance, expanding the Medicaid entitlement, and cooking up a witch’s brew of new taxes and mandates. The focus of the law was expanding coverage, not controlling costs or improving quality, which would have required disrupting heavily regulated and subsidized sectors of the pre-ACA system, such as Medicare and employer-sponsored health insurance.

All that to say: Obamacare was far less disruptive than what we needed. If you want to know what disruptive health care policy looks like relative to Obamacare, the Manhattan Institute’s Avik Roy this week published an eminently credible and detailed plan to drastically reshape Obamacare and in the process cure many of the ailments that plagued our pre-ACA system. The plan, aptly named the Universal Exchange Plan, purports to cover 12 million more Americans by 2025 than what the ACA is projected to cover, produce a net deficit reduction of $8 trillion, lower the cost of private health insurance, and render Medicare permanently solvent.

Stop Controlling People

The centerpiece of Roy’s plan is the deregulation of the health insurance exchanges at the heart of Obamacare. Freed from onerous restrictions on what kinds of health plans they can offer, insurers could furnish a wider range of coverage options that would be more attractive to younger Americans, who have so far been reluctant to sign up for costly and overregulated Obamacare exchange coverage. Poorer Americans would still receive subsidies to purchase coverage, but on an amended sliding scale based on income, with extra incentives to choose a high-deductible plan coupled with a health savings account. Eventually, Medicaid and Medicare would be folded into these reformed exchanges under a “premium support” model, with more Medicare dollars going to poorer seniors and less going to the middle and upper class. Meanwhile, the individual and employer mandates would be repealed, as would all the new Obamacare taxes on health plans, medical devices, and all the rest.

Those with employer-sponsored coverage would feel the least disruption under the Roy plan, and would likely see their medical bills decrease as a result of more competition between hospitals, the growth of health savings accounts, increased use of telemedicine, medical tourism, and malpractice reform, among other things. At the heart of all these changes is the goal of creating a consumer-driven health care system, which Roy believes could improve care for poor Americans, reduce the cost of care for everyone, and “put America’s finance’s on a permanently stable course.”

For all its market-based reforms, Roy’s plan does retain some contentious regulatory features of the ACA, like the “Cadillac Tax” on high-cost employer plans, under the theory that the employer tax exclusion is “the largest entitlement in the tax code and the second-largest entitlement—next to Medicare—overall.” (Roy notes Congress could achieve the same result simply by imposing a fiscally equivalent cap on the size of the employer tax exclusion). Insurers would still be required to cover those with pre-existing conditions and be prohibited from charging different rates based on health status—known as “guaranteed issue” and “community rating,” respectively. But Roy’s plan relaxes the ACA’s age-rating restrictions by allowing insurers to charge older Americans up to six times what they charge younger people (the ACA’s limit is three to one).

To be sure, conservatives will find a lot to complain about in all of this, and not just because it doesn’t repeal every piece of Obamacare. In some areas, it continues to rely on government funding for healthcare, which for some people is and always will be unacceptable. But what’s much more important—and this is what Roy gets right in a way that no one else has yet—is that the plan addresses, in a substantive way, those features of the American health care system that have been driving up the cost of care, and eroding its quality, for half a century.