Senators are supposed to represent the people who live in their states. But on repealing Obamacare, four Republican members of that august body seem not to know their constituents very well.

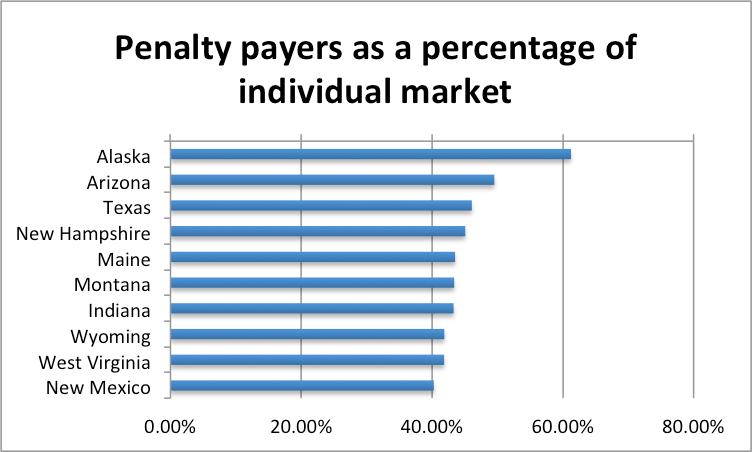

Three have consistently voted to keep the Affordable Care Act in place: Lisa Murkowski (AK), Susan Collins (ME), and Dean Heller (NV). A fourth, John McCain (AZ), has crossed the aisle once. Interestingly, in 2015 three of those states were among the top ten in which residents eligible to purchase individual policies chose instead to pay the tax.

Alaska is number one, with 61.2 percent of those eligible paying the penalty. Arizona is number two, at 49.5 percent. Maine occupies fourth place, with a 43.5 percent rebellion rate. Nevada weighs in at the number 15 slot, with 38.1 percent refusing to share responsibility. Here are the top ten states.

Part of the current tax bill wending its way through Congress repeals the individual mandate to purchase health insurance. This is a particularly noxious part of the “Affordable” Care Act (ACA), in that it forces taxpayers to purchase a product. To enforce this mandate, the Internal Revenue Service is empowered to collect an “individual responsibility fee”—essentially a tax penalty levied on those who don’t buy health insurance.

Even the Supreme Court Says It’s a Tax, Remember?

In an entertaining side note to the ongoing debate, Democrats objected that Republicans are inserting health care into the tax bill with individual mandate repeal. “My understanding is the individual mandate is a tax,” replied Sen. John Thune (R-SD), referencing the (in)famous SCOTUS decision. Chief Justice John Roberts joined the four liberal members of the court in ruling that the penalty for not buying health insurance was, in practice, a tax. From SCOTUSblog:

Here is the choice that individuals who do not want to obtain health insurance will face, according to the Chief Justice: ‘Those subject to the individual mandate may lawfully forgo health insurance and pay higher taxes, or buy health insurance and pay lower taxes. The only thing they may not lawfully do is not buy health insurance and not pay the resulting tax.’

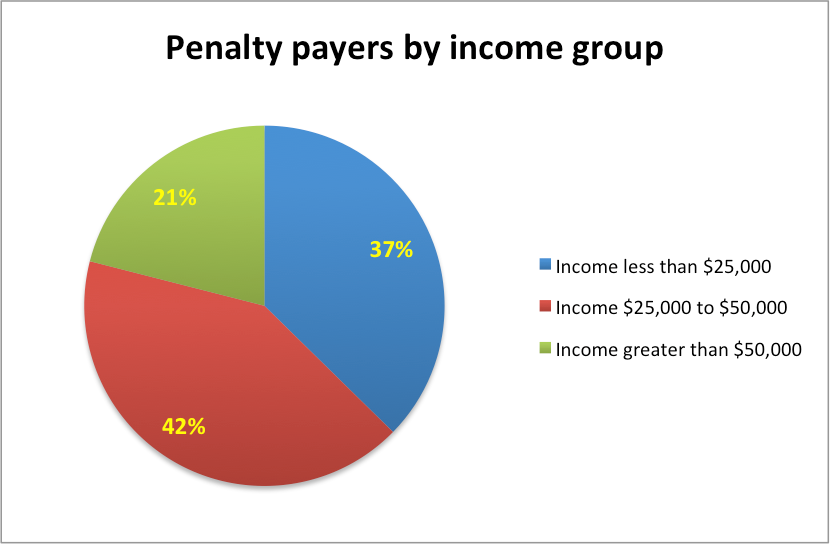

One ACA goal was to extend health insurance to low-income households. Ironically, many of the households who choose to pay the penalty are those same low-income households. Now, it’s possible these folks simply don’t understand that there may be subsidies available for them to purchase insurance. But, given that the tax penalties were set so low, it seems far more likely that it’s simply cheaper to pay the tax.

The IRS recently released data for 2015. The table included a state by state breakdown of the number of people paying the penalty, the total amount collected, and, for income ranges $0 to $25,000 and $0 to $50,000, the number and percentage of those paying the penalty. Let’s start by looking at the results for the whole country.

More Low-Income Folks Choose the Tax Over Insurance

For the United States as a whole, 6,665,480 taxpayers paid a total of $3,079,255,000 in penalties. That’s an average of $461.97 per person. Of that group, 37.35 percent (2,489,490) had incomes of less than $25,000 per year. An additional 2,774,890 had incomes between $25,000 and $50,000.

In total, 78.98 percent of those who paid the penalty had income less than $50,000. If we repeal the mandate, these folks will get an immediate tax cut equal to the amount of the penalty they paid. Assuming each receives the average penalty, the total tax cut will be $2.4 billion. While that’s not enough to stimulate a $20 trillion economy, it’s a move in the right direction.

According to my calculations, there were 204.8 million U.S. taxpayers in 2015. They filed a total of 150.5 million returns. (Remember, those who file joint tax returns count as two taxpayers.) Only 3.25 percent of taxpayers paid the ACA penalty. However, that number vastly understates the magnitude of the situation. Most taxpayers get health insurance through either their employer or some employment-related entity, such as a union.

According to the Kaiser Family Foundation, 156 million individuals are covered by employer-based insurance. An additional 6.4 million have military or Veterans Affairs coverage. Medicaid covers 62.4 million, and Medicare handles 43.3 million. And 29 million are uninsured.

That leaves 21.8 million in the “non-group” category. Sadly, that includes both those who bought their own insurance and those covered as a dependent on someone else’s policy. It would be nice to separate those two groups. Then we would have a more accurate figure for those who bought their own insurance. But the current state of the data doesn’t allow it.

Let’s make an extreme assumption. Consider the population between ages 18 and 65. Under U.S. law, you are strongly encouraged to sign up for Medicare when you turn 65. Failure to do so creates severe, long-lasting penalties. So let’s assume that the proportion of those covered as dependents is equal to the number of people between ages 18 and 26 divided by the population between 18 and 64. (The ACA kicks children off their parents’ policy on January 1 of the year following the year when they turn 26. Who in the world dreams up rules like this, anyway?) Since we’re making some pretty extreme assumptions here, I’ll just include all 26-year-olds in the 18-26 group.

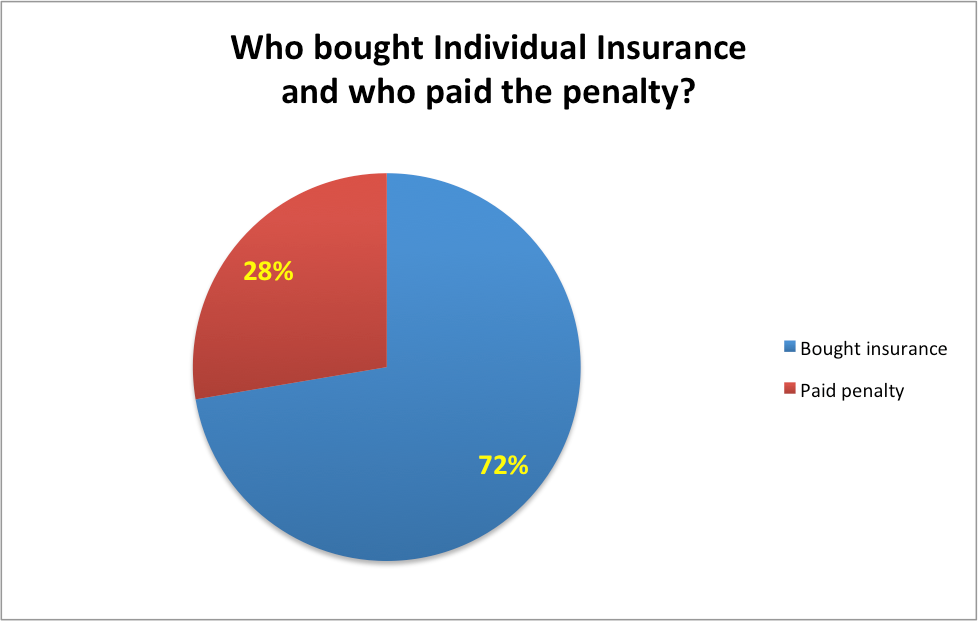

Using population data broken down by age (year by year) and state, we can do those calaculations. In 2015, there were 39,868,558 U.S. people between 18 and 26. There were 158,481,553 between 27 and 64. That means 79.9 percent of the population between 18 and 64 was also between 27 and 64.

Applying that percentage to the KFF “non-group” total of 21,816,500 implies 17.4 million people bought insurance through the ACA. Adding the 6.7 million who paid the penalty gives 24 million people who were eligible for individual insurance. Of those, 27.7 percent chose to pay the penalty.

The poor pay a disproportionate percentage of this Obamacare tax penalty. Repealing the individual mandate gives these folks an immediate tax cut. If lawmakers really want to help the poor, they should do this sooner rather than later.