An expansive new study on the Federal Reserve’s quantitative easing (QE) program found that QE’s ultra-low interest rates have enriched banks and central governments at the expense of households and pensioners. The study, which was conducted by the consulting firm McKinsey & Company, examined the distributional effects of the change in interest rates that resulted from QE’s bond-buying program. The lower rates almost certainly helped net borrowers, who were able to take advantage of lower borrowing costs, and hurt net savers, who were punished with lower rates of return on their investments.

“These distribution effects are most likely unintended consequences of central bank policies,” the study’s authors wrote. “Lower rates have reduced interest payments for borrowers but have diminished the interest income of savers.”

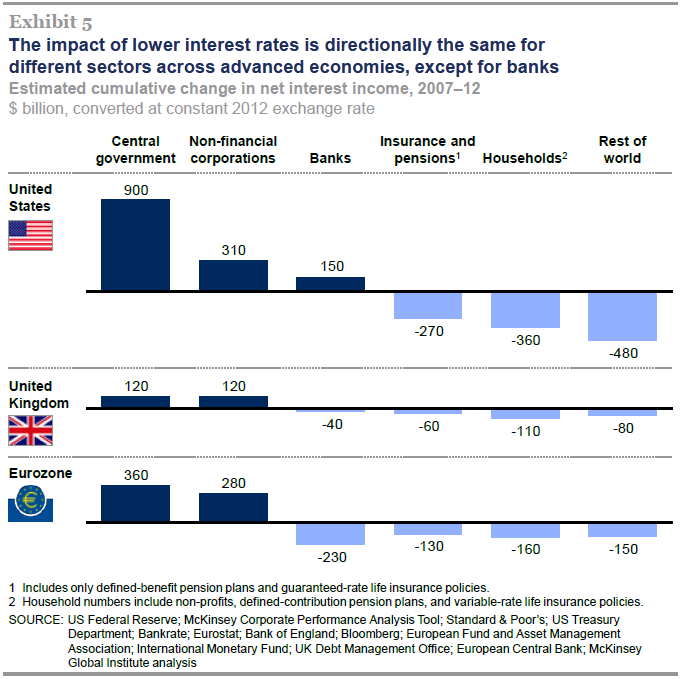

McKinsey analyzed the interest incomes and expenses of various sectors in 2007 and 2012 and estimated how much of the changes could be attributed to the Fed’s QE program.

According to the study, the U.S. central government was by far the biggest QE beneficiary, with cumulative net interest benefits of $900 billion. Non-financial corporations received $310 billion in benefits, while U.S. banks received $150 billion. The biggest losers were American households, which lost $360 billion due to QE’s effects, and life insurance and pension plans (most of which have individuals or families as beneficiaries), which lost an additional $270 billion.

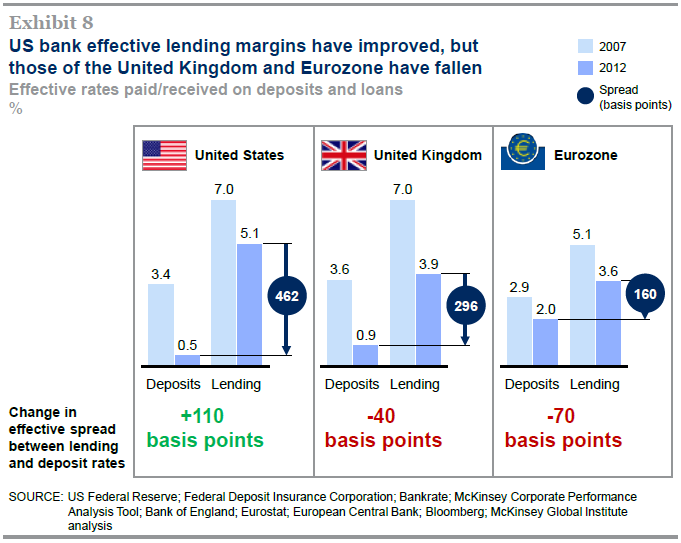

Banks were a large beneficiary of QE because of the policy’s effect on the spread between a major bank’s cost of borrowing (which approached zero under QE) and its returns from lending (which did not fall as much as borrowing costs). In total, QE increased the banks’ overall profit spreads by 110 basis points, or 1.1 percent, as effective borrowing costs fell by nearly 3 percent while effective lending returns fell by only 1.9 percent.

“Banks in Europe have experienced a large decline in net interest margins in this era of ultra-low interest rates, but that has not been the case in the United States,” the study found. “Long-term investors such as pension funds and life insurance companies, as well as households, have lost net interest income because they hold far more interest-bearing assets than liabilities.”

The study also found that QE was responsible for 20 percent of the profit growth of U.S. non-financial corporations since 2007. And those additional profits were concentrated among large firms, with few of the benefits trickling down to small businesses.

“Large corporations have secured particularly large benefits because they are able to issue bonds in debt capital markets and have continued to be able to access bank loans,” McKinsey found. “However, many small companies across advanced economies — and even some larger ones in Eurozone periphery countries — have not been able to access lower-cost credit because they have been more reliant on bank loans for financing.”

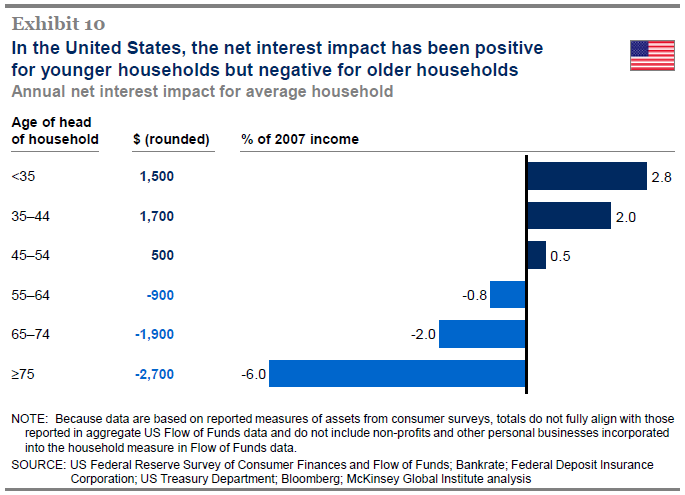

McKinsey’s analysis also found that QE enriched younger households at the expense of older households, especially those older households approaching or at retirement. This was due to the fact that younger households are likely to have more debt, while older households are likely to have more savings. The losses to the older households, however, swamped any gains reaped by the younger households, as older losses exceeded younger gains by $1.8 trillion.

But surely the household savings losses from the lower rates would be more than offset by higher asset prices resulting from the rate changes, right? Not so much, says McKinsey.

“Increases in bond prices are merely the flip side of falling interest rates, creating apparent gains for investors who mark their bond portfolios to market, but we find little evidence that ultra-low interest rate policies have boosted equity prices in the long term,” McKinsey found. “In the United States, the evidence on whether action by the Federal Reserve has lifted the housing market is also unclear, because it is difficult to disaggregate the impact of these measures from other forces at work in the market.”

“Taking everything into consideration,” the asset price analysis concludes, “the theoretical and empirical evidence on the impact of QE and ultra-low interest rates does not point conclusively to an increase in equity prices.”