There are many things that might have been done to reform health care in the United States after Barack Obama was elected. Lord knows our system needs it. The Affordable Care Act does begin to address some of these problems:

- It begins to break the bond of employers being the primary provider of health insurance coverage. This was always an odd idea that exists as an artifact of the wage and price freeze of World War Two. Employers were not allowed to raise wages to attract workers, so they began offering “fringe” benefits instead. The wage controls lingered into the post-war boom years long enough for health benefits to become a fixture of the workplace. Obamacare relieves smaller employers (under 50 workers) of any expectation of providing coverage, and gives larger employers an affordable way out.

- It begins to move away from the regressive tax subsidy available solely through employers and perversely benefitting higher incomes and richer benefits. The value of employer-provided health benefits is “excluded” from income, so it is completely free of any taxes, state or federal, income or payroll. There is no limit on the value of those benefits, so the current tax law encourages ever-richer insurance, and people in higher tax brackets get far more assistance than those with lower incomes. There is no similar advantage offered to health benefits purchased by individuals. Obamacare offers lower-income people in the private market some tax assistance, too, through income-based premium assistance.

- It embraces on-line marketing that is independent of insurance company-paid commissions through its health insurance exchanges. Currently agents and brokers are paid commissions on the insurance products they sell. This is not to say they don’t provide valuable services to their clients, but there remains an incentive for them to direct clients to the companies that pay the highest commissions. The concept of on-line marketing is a good one, even though the specific approach and implementation of the Obamacare exchanges has been horrific.

If Obamacare had confined itself to these three reforms we would all be applauding it and working to help improve it. Unfortunately, health reform has long been tainted by the bumper sticker slogan of “universal health insurance” in the minds of most Democrats. If health reform did not include universality it was not worth pursuing, in their view.

How can Democrats make sure it is universal? Simple. Pass a law mandating that everyone must buy it or be punished! Problem solved. No sweat.

Alas. Things are never that simple.

In an enormous, dynamic, and fluid nation like ours it is impossible to get “everyone” to do anything. It doesn’t matter the size of the penalty. It doesn’t matter how easy compliance might be. There is always a contingent of the population that won’t do it.

Studies have been done about compliance with helmet laws, seat belt laws, laws against using cell phones while driving, speed limit laws, child support laws, auto insurance coverage, even tax laws. About fifteen percent of the population won’t comply. In some cases the penalties are severe, like jail time. Still, 15% are in violation.

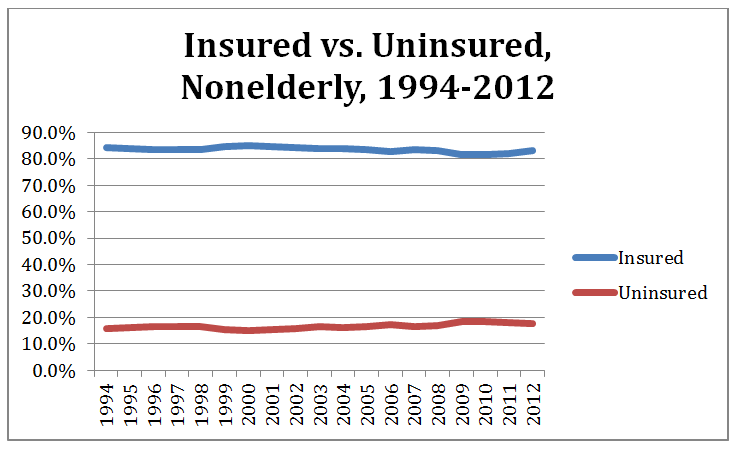

Interestingly, this is about the same as the rate of non-insurance for health care in a voluntary market. The graph below is from the most recent report on insurance coverage by the Employee Benefit Research Institute (EBRI). It is based on Census Bureau numbers from 1994 through 2012. Every year about 84% of the non-elderly population has health insurance coverage and 16% does not. The number wobbles a little bit during recessions, but not by much. It doesn’t matter how many new programs are enacted, how many new incentives are offered, or how much the cost of coverage goes up, the percentages stay the same. One would be hard-pressed to find a more stable “trend” in any area of our economic lives.

In the case of health insurance, there is a good-sized portion of the population that is incapable of managing it. They might be illiterate or mentally ill or drug addicted or in the underground economy or simply have poor impulse control. They can’t read a contract, can’t keep an appointment to see a doctor, and can’t follow prescribed treatment programs.

These folks don’t need insurance, they need a source of health care services. They will wait till they feel poorly and roll down to the emergency room like they always have because that is where the doctors are. In Massachusetts the use of emergency department services went up, not down, after the mandate went into effect there.

Even a public insurance program like Medicaid isn’t the answer. Some one-third of the uninsured are already eligible for Medicaid but simply haven’t enrolled. A study a few years ago in the journal Health Affairs found that one-third of all children eligible for Medicaid or S-CHIP had been enrolled in the program in the previous year but their parents didn’t bother re-enrolling them. It wasn’t that they didn’t know about it or they didn’t know how to enroll. They simply weren’t motivated to do it.

What About “Free Riders?”

Obviously these people will continue to receive care whether they are insured or not, so the primary rationale for mandatory coverage – solving the “free rider” problem – will not be solved. Yes, it may be reduced, but it would be reduced anyway if the subsidies were available without a mandate. More people would buy insurance on a voluntary basis because more people could afford it..

And uncompensated care (“free riding”) is not an enormous problem in any event. Most serious studies place it at about 3% of total health care costs. This is not much different than the losses to retailers from shoplifting and employee theft. It is just a cost of doing business in a free society.

Further, while uncompensated care may raise costs for the insured, those costs do not disappear with a mandate. They are simply transferred over to the tax system and used to subsidize coverage rather than subsidizing the care itself.

Indeed, if we consider all of the federal subsidies paid out to various people, the costs to taxpayers makes the cost of uncompensated care seem trivial. The American Hospital Association estimates that uncompensated care cost hospitals $41 billion in 2011, while the Urban Institute estimated the exclusion from taxes of employer-sponsored health insurance alone cost the federal government $268 billion in foregone revenues. Throw in subsidies provided for Medicare, Medicaid, and hundreds of other federal programs, the money you pay to subsidize other people through your taxes are massive compared to the extra premiums you might pay for uncompensated care.

What should be done?

The goal of making health insurance coverage more affordable and more accessible is a good one, even if it will never be universal. So what should be done?

First, we should look at the uninsured as an untapped market with varying needs, preferences, and resources, instead of as unified block of helpless supplicants. Rather than treating them like criminals for not doing what we think they should, we should treat them like potential customers. If they don’t like what is currently available, perhaps that is more of a commentary on the products than on the people who don’t buy.

And in fact the uninsured are a varied lot – 59.9% of them are workers, 26.1% are not, and 13.9% are children. Of these workers, 21.1% are employed by very small firms (fewer than 10 employees), but another 21.1% work for companies with 1,000 or more employees: 29.2% are in service jobs, 21.6% are in sales or office work, but 17.6% work in “managerial or professional” capacities according to the EBRI report cited above.

Even more interesting is the family income level of the uninsured:

- 8.0 million earn under $10,000

- 7.7 million earn from $10,000 to $19,999

- 7.7 million earn from $20,000 to $29,999

- 6.1 million earn from $30,000 to $39,999

- 4.4 million earn from $40,000 to $49,999

- 6.7 million earn from $50,000 to $74,999

- 6.9 million earn over $75,000

As interesting as the demographic breakdowns are, the “psychographic” profile is even more enlightening. Three years after enactment of the law, CMS decided to finally ask the question: just who are these poor wretched uninsured people and what are they looking for? One might think they would have inquired about this before enacting a remedy, but there you have it.

Turns out 92% of them can be divided into three segments:

The biggest cluster (47.8% of all the uninsured) are “healthy and young.” They are not much motivated to enroll and they take their health for granted.

The next largest group (28.9%) are “sick, active and worried.” These tend to be older and are pretty good candidates for coverage.

Finally we have the “passive and unengaged” group (15.3%). These folks tend to be older and have poor literacy skills.

These different people need different solutions.

The first group is unlikely to want to spend a lot of money on services they can’t foresee needing. But they might like a Health Savings Account that allows them to be protected against catastrophe, while building up a sum of money for the future when they are more likely to need it.

The middle group would probably embrace comprehensive coverage if their expenses could be subsidized and they were assured of getting coverage.

The final group is made up of the people we wrote about above. They are not capable of understanding or navigating any health insurance system. They need the direct provision of care through neighborhood clinics and subsidized hospitals.

Unfortunately, the Affordable Care Act seems to be aimed solely at the middle group – the 29% of the uninsured who are sick and worried. This is the stereotype rolled out by politicians who want to show off how much they care.

But their compassion seems to extend only to less than a third of the 16% of the population currently without insurance coverage – i.e. about five percent of the American population. So 95% of the country is being put through the wringer to benefit the 5% this law was written for.