Recently when the EpiPen was the epicenter of the pharmaceutical pricing controversy, the media and politicians predictably painted maker Mylan and its CEO, Heather Bresch, as the villains.

In the battle between Big Pharma and its true opponents—Big Insurance and Big Government—I don’t have a dog in the fight, although as I have implied on Twitter, if forced to choose, I’d rather root for the guy who makes money when people live than the one who does when people die. But what does matter to me is whether sound bites prevent an honest dialogue about the causes of high drug prices and the consequences of government intervention.

Yes, It’s Fair to Blame Obamacare

The discussion of drug pricing typically ignored Obamacare’s role in burdening EpiPen users’ finances. Thanks to Obamacare’s mandates, more employers have opted for high-deductible insurance plans, which typically boast lower monthly premiums. Adam Rubenfire recently highlighted this trend: “About 24% of workers in employer-sponsored plans were enrolled in a high-deductible plan linked to a health savings account in 2015, compared with 20% in 2014 and just 4% in 2006.”

Under these plans, enrollees must pay out-of-pocket expenses—sometimes up to $6,000 or more—before insurance kicks in. Individuals covered by high-deductible plans thus faced paying the entire $600 wholesale price for the EpiPen until they satisfied their deductibles. The high price of the EpiPen also hits harder those with high co-pays.

Here, too, Obamacare has a hand in the problem: in an effort to keep costs low and, in turn, premiums, insurance companies increased insureds’ co-pay share. These changes hit consumers as the price of the EpiPen escalated, magnifying the problem for cash-strapped patients. In discussing the EpiPen controversy, USA Today’s headline captured this dynamic perfectly: “EpiPen’s steady price increases masked until deductibles rose.”

After a week of public shaming, Mylan announced its first response: expanding its financial assistance programs. Mylan will now provide $300 to help offset the EpiPen’s cost. In announcing its initial change, Mylan also highlighted Obamacare’s role in the controversy: “As the health insurance environment has evolved, driven by the implementation of the Affordable Care Act, patients and families enrolled in high deductible health insurance plans, who are uninsured, or who pay cash at the pharmacy, have faced higher costs for their medicine.”

Critics pounced. See this headline from Time magazine.

It is true that Obamacare is not responsible for EpiPen’s high wholesale price, although the government does share some responsibility for that as well, as Scott Gottlieb has explained. But attacks on Mylan’s EpiPen pricing all focused on those at risk for anaphylactic shock. Here Obamacare does bear responsibility. It altered the insurance market such that this life-saving drug became cost-prohibitive to a large swath of users.

Prior to Obamacare, the EpiPen’s escalating price didn’t affect most consumers. Doug Hirsch, co-CEO of drug comparison site GoodRx, explained this dynamic to NBC News, stating: “When consumers perceive that the cost of drugs is going up, often it’s just their share of the costs that are going up. … We see that all the time at GoodRx.”

Fighting Over Whom to Stick with the Tab

Obamacare caused that change. And to pass Obamacare, the government got into bed with insurance companies. Now that they find themselves pregnant, they point elsewhere—Big Pharma. But by expanding its consumer assistance programs, Mylan deflected the most devastating attack against its EpiPen pricing: innocent allergy suffers will now have access to this life-saving medication, either at no or low cost. Insurance companies and taxpayers in general (through Medicare and Medicaid) will instead bear the cost.

Recognizing that public outcry is unlikely when Big Pharma is pitted against Big Insurance and Big Government, Hillary Clinton pivoted back to the individual, with her campaign spokesman Tyrone Gayle explaining: “Discounts for selected customers without lowering the overall price of EpiPens are insufficient, because the excessive price will likely be passed on through higher insurance premiums.”

Ironically, under the guise of reining in Big Pharma, Clinton has proposed limiting out-of-pocket payments for drugs to $250 a month; her proposal will also raise premiums by increasing costs to insurance companies. That is why Big Pharma supports this legislation and Big Insurance opposes it.

Further, the increase in premiums could be substantial. Sally Pipes highlighted the 3 percent increase in premiums for California residents after the state adopted out-of-pocket caps.

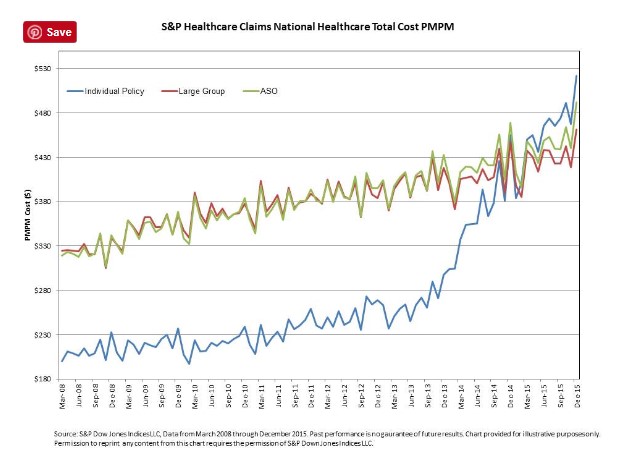

Notwithstanding the irony of Hillary’s latest salvo at the pharmaceutical industry, she is of course right that drug prices affect insurance premiums. But here too Obamacare holds more responsibility than Mylan. Brian Blase details the impact, including the two-year 69 percent increase in per member per month (PMPM) costs between 2013 and 2015. Conversely, EpiPen’s effect on premiums appears slight, with one calculation showing a PMPM of only two cents.

Another irony—one the public has yet to grasp—is that while pharmaceutical companies are the ones condemned as uncaring, the health insurance industry does not want pharmaceutical companies to subsidize patients because that encourages overconsumption, especially of costlier drugs. Health insurance companies first sought to discourage customers from using high-cost drugs with tiered co-pay systems: for more expensive drugs, consumers bore high co-pays.

But then consumers with pharmaceutical discount cards could obtain reimbursement for out-of-pocket expenses, negating the financial incentive for them to consume less-expensive drugs. Insurance companies responded by excluding drugs from their formularies of covered drugs. So prevalent are formulary exclusions now that DrugChannels.net, which reports on pharmaceutical economics, created its own “Join the Party” meme.  But where there are no, or few, other options—as with the EpiPen—high deductibles or co-pays discourage consumption to the benefit of the health insurance company. Mylan’s discounts thus did not placate the health insurance industry.

But where there are no, or few, other options—as with the EpiPen—high deductibles or co-pays discourage consumption to the benefit of the health insurance company. Mylan’s discounts thus did not placate the health insurance industry.

Mylan Upstages Politicians and Big Insurance

Mylan’s second response to the controversy broke on Monday, when it committed to bringing a generic version of the EpiPen to market within weeks at a list price of $300. This adds a further twist to the narrative. By offering a generic version at half the price, Mylan presents itself as having responded to the uproar.

Insurance companies, however, will likely respond by limiting coverage to the generic version. All other things being equal, consumers prefer name-brands to generics. If deprived of their preferred product, consumers will view the health insurance companies as the bad actor.

Mylan’s move will also cement itself as the long-term go-to provider of epinephrine auto-injectors just as competitors were about to reach the market with a generic version. As Business Insider aptly explains, offering an authorized generic is “basically a drugmaker’s way of staying in the game after generic competition comes to the market.”

In short, Mylan’s two-prong response has played politicians and the health insurance industry like an iPad in the hand of a basement-dwelling millennial. Such gaming, though, was only possible because the health insurance industry’s complexity and media and politicians’ sound-bite strategy enabled Mylan to defeat the latter by understanding the former. Only when politicians, the media, and the public acknowledge the intricacies and competing interests at play in the pharmaceutical and health insurance industries will we all find better solutions.

Disclosures: The author’s family 401(k) and retirement savings include diverse holdings, including mutual funds in both the health-care and pharmaceutical sectors; it also includes immaterial investments in several individual biotech stocks.

Previously this article stated “ephedrine auto-injectors” instead of “epinephrine auto-injectors.”