Well, that didn’t last long. Fewer than six months after Congress effectively repealed Obamacare’s individual mandate—and more than six months before that change actually takes effect, in January next year—another liberal group released a plan to reinstate it. The proposal comes as part of the Urban Institute’s recently released “Healthy America” plan.

In the interests of full disclosure: I criticized Republicans for repealing the individual mandate as part of the tax reform bill last fall. I did so not because I support requiring Americans to buy health insurance—I don’t—but because Republicans need to go further, and repeal the federal insurance regulations that represent the heart of Obamacare and necessitated enacting the mandate in the first place.

Conversely, the Urban Institute plan would push Obamacare’s already onerous regulatory regime much further to the left, restoring the mandate—and many more federal requirements.

Lipstick on an Unpopular Pig?

The Urban Institute plan tries to re-brand a federal requirement to purchase insurance by never even using the term “mandate” in its proposal. Instead, the document says that “uninsured people would lose a percentage of their standard deduction (or the equivalent for the itemized deduction) when they pay income taxes….Half the lost deduction amount could be refunded the following year if the person enrolls in coverage and maintains it for the next full plan year.”

But as the saying goes, if it looks like a mandate and functions like a mandate, it’s a mandate. The paper claims that taking away a “tax benefit…would be better received politically than the additional tax penalty” under Obamacare, but functionally, that provides a distinction without a difference. Even the Urban researchers call this “loss of a tax benefit” a “penalty” later in the paper, because that’s what it is: A penalty for remaining uninsured.

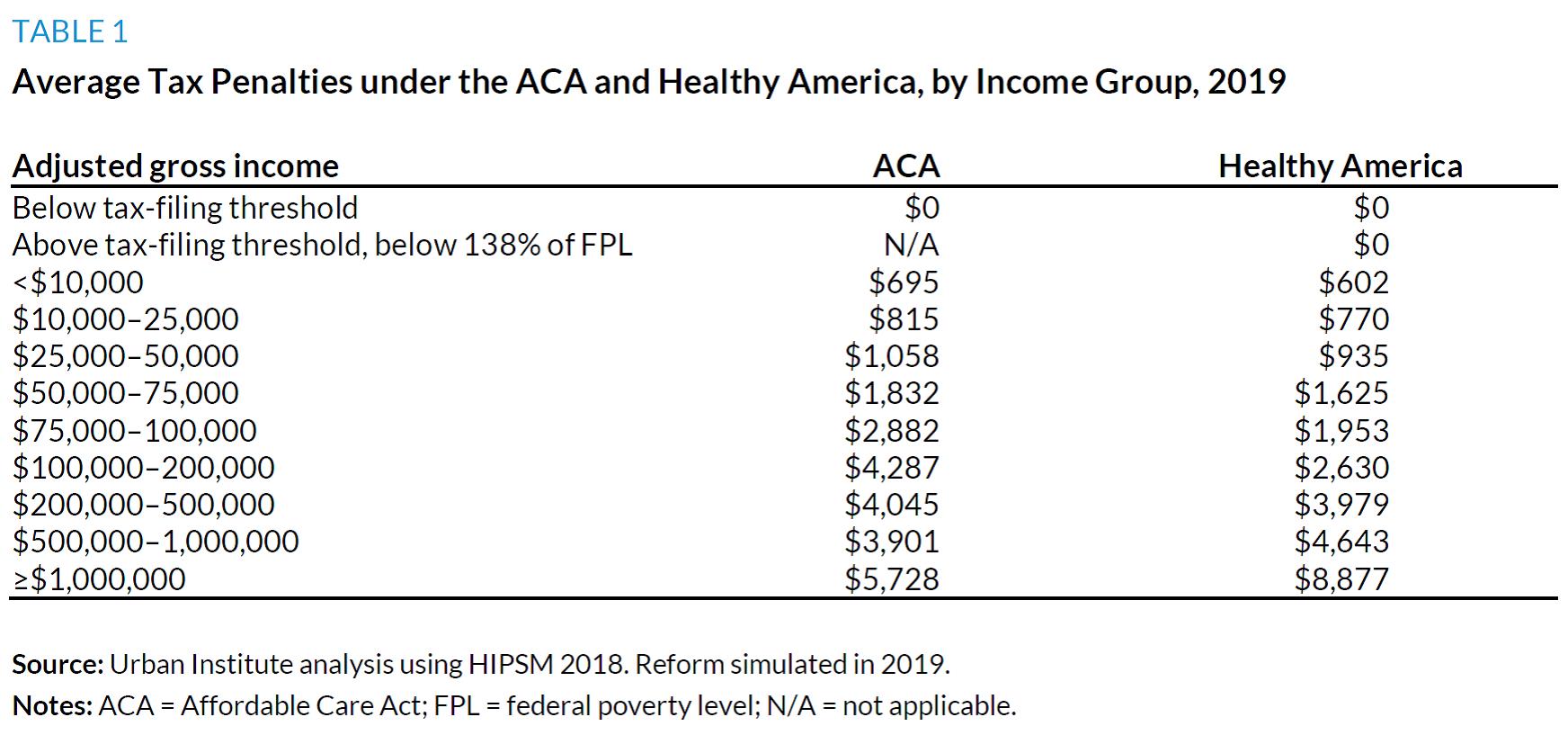

The paper even includes a chart highlighting the average tax for remaining uninsured by income under the proposal, which generally mimics the tax penalties the uninsured pay under Obamacare:

Other Components of the Plan

Unfortunately, the Urban Institute plan goes well beyond merely reinstating the individual mandate, albeit in a slightly different form. It also makes other major changes to the health care system that would entrench the role of the federal government in it. It would federalize Medicaid health insurance coverage by transferring Medicaid enrollees into exchanges, supplementing benefits for low-income children and individuals with disabilities, and requiring states to keep paying their current contributions into the system. (Long-term care coverage under Medicaid would continue unchanged.)

The exchanges would have a new government-run plan—the default option for low-income enrollees automatically enrolled into coverage—and options run by private insurers. However, all plans would cap reimbursement to doctors and hospitals at Medicare rates, making premiums more “affordable” by imposing price controls that would potentially pay providers at below-market levels. The plan also proposes to “save” on prescription drugs by extending Medicaid rebates (i.e., price controls) to additional individuals.

The Urban plan also proposes much richer health coverage subsidies, consistent with its earlier 2015 proposal. Specifically:

- Individuals with incomes below the federal poverty level would not pay either premiums or cost-sharing;

- Individuals with incomes below 138 percent of poverty (the threshold for Obamacare’s Medicaid expansion) would not pay premiums;

- Premium subsidies would be linked to a plan paying 80 percent of expected health care costs (i.e., actuarial value), as opposed to a 70 percent actuarial value plan under Obamacare;

- Individuals would have to pay less of their income in premiums than under Obamacare—for instance, an individual with income just under four times poverty would pay 8.5 percent of income in premiums, as opposed to 56 percent under Obamacare; and

- Unlike Obamacare, which limits eligibility for subsidies to those with incomes under four times poverty, the Urban plan would limit premium payments to 8.5 percent of income at all income levels (i.e., including for those making more than four times poverty).

The Urban Institute plan does not abolish employer-based insurance outright. However, because the plan 1) eliminates Obamacare’s employer mandate, 2) abolishes the “firewall” that prevents individuals with an offer of employer coverage from obtaining federal insurance subsidies, and 3) caps premiums as a percentage of income at all income levels, many employers could decide to drop coverage and send their workers to exchanges.

Moreover, “short-term and other private insurance plans that do not comply with Healthy America regulations (consistent with [Obamacare’s] regulatory framework” would be prohibited, including association health plans and other concepts the Trump administration has proposed to give Americans more flexible coverage options.

The Urban researchers admit their plan would require significant new revenues to pay for the new subsidies—an estimated $98 billion in the first year alone. The plan only briefly discusses options to pay for this new spending, but it admits that, even if Congress hikes the payroll tax by an additional percent, raising an estimated $823 billion over ten years, “other adjustments to excise and income taxes would be needed.”

Where the Plan Fits In

At the end of their paper, the Urban researchers include a helpful chart comparing the various liberal proposals for expanded government involvement in health care—lest anyone claim that the left hand doesn’t know what the far-left hand is doing. In general:

- Elizabeth Warren (D-MA) introduced a bill that would not go as far as the Urban plan. It incorporates the subsidy changes Urban proposed, adds a government-run plan, and imposes other regulatory changes to the exchanges, but (unlike the Urban plan) retains the status quo for Medicaid;

- The Center for American Progress’ “Medicare Extra” proposal, which I wrote about earlier this year, goes farther than the Urban plan, by eliminating Medicaid (which the Urban plan modifies) entirely, and including more robust auto-enrollment provisions, with “Medicare Extra” the default option for all Americans; and

- The single-payer bill introduced by Sen. Bernie Sanders (I-VT) would go farthest of all, abolishing virtually all forms of insurance (including Medicare) and creating a single-payer health system.

It says much about the leftward shift of the Democratic Party that the government-run “public option” represents the most conservative of all the policy proposals discussed. It also says much that the Urban Institute estimates “only” 18.3 million individuals would lose their employer-sponsored coverage under their plan. That’s roughly four times the number of individuals who received cancellation notices when Obamacare took effect in 2014.

So much for “If you like your plan, you can keep it.” For that matter, so much for “If you like your freedom, you can keep it.” Like it or not, the Left seems insistent on terrifying the American public with what Ronald Reagan viewed as the nine most effective words to do so: “I’m from the government and I’m here to help.”