Like President Obama’s now-infamous line from 2009 that, “If you like your health care plan, you can keep your health care plan,” which isn’t quite accurate, the administration’s claim that coverage under Obamacare will somehow be cheaper is also proving not quite true for many people—especially the young and healthy.

Since the rocky launch of the exchanges on October 1st, Americans have (through great effort) been getting glimpses of what premium rates will be for ACA-compliant plans. Turns out, the plans aren’t cheap. (Recall that the president promised in 2008 that his health care law would “lower premiums by up to $2,500 for a typical family per year.”)

This is especially true for states like Texas, which prior to Obamacare had a lightly regulated individual insurance market where relatively young, healthy Texans could get high-deductible, catastrophic coverage for about $60 a month. With the advent of Obamacare, those days are gone.

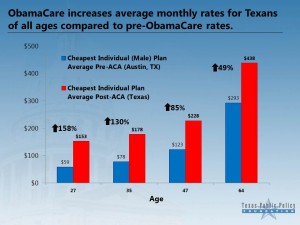

Here at the Texas Public Policy Foundation, we examined pre- and post-ACA rates on the individual health insurance market in Texas, and found that some Texans will pay on average 158 percent more for the cheapest plan on the federal exchange than they would have paid prior to Obamacare. A 27-year-old in Austin, for example, could have bought a catastrophic plan for $59 a month before the ACA. On the exchange, the cheapest catastrophic plan is $153 a month.

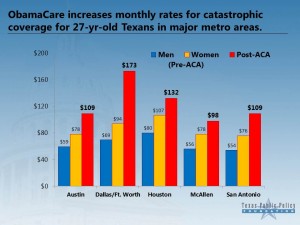

One reason we looked at catastrophic plans is because in most cases they are available only to people under age 30—the very group that the administration has said needs to sign up in large numbers for the exchanges to work. The other reason we compared pre- and post-ACA catastrophic plans is because such plans are not eligible for federal subsidies, so the higher costs on the exchange must be paid be the plan enrollee entirely out of pocket. Although costs vary throughout the state, and premium hikes are worse for men than for women, the trend is consistent: in every major metropolitan area of Texas, rates on the exchange are higher.

Obamacare supporters will say, as they have about other attempts to compare pre- and post-ACA rates, that it’s impossible to do this because ACA-compliant plans have more benefits, limit out-of-pocket costs, and don’t discriminate based on gender or pre-existing conditions. But it’s precisely because of these features that coverage on the exchanges is so much more expensive for young, healthy people.

Americans who purchase coverage on the individual market will want to know, above all else, how much they must pay. In Texas, a wide swath of people will have to pay more, period. Of course, premium rates vary widely depending on age, location, and income. But consider the following examples, cited in our paper:

- A 27-year-old Houston resident earning 250 percent FPL, or about $28,725 annually, will only qualify for a subsidy of $8.40 a month, leaving more than $192 in out-of-pocket monthly costs for the second lowest-cost plan on the exchange.

- A 27-year-old making $30,000 a year in Austin will not qualify for any federal subsidy at all, and will have to pay about $109 a month out-of-pocket for a low-cost catastrophic plan on the exchange, amounting to more than $1,300 annually.

- A 35-year-old Texan who earns $30,000 a year will be eligible for annual subsidies that amount to a mere $201, leaving average out-of-pocket annual costs for the second lowest-cost silver plan in Texas at more than $2,500.

A 40-year-old San Antonio resident earning 300 percent FPL ($34,470) does not qualify for a subsidy and will pay an annual premium of approximately $2,871 out-of-pocket for the second lowest-cost silver plan on the exchange.

What this sampling shows is that the group of people the administration needs to sign up for exchange coverage—healthy, working people in their 20s and 30s—have the least incentive to do so.

Pointing this out and examining the numbers as we’ve done is not in itself an argument against Obamacare. It is merely an observation of a reality that has too often been overlooked in the debate over Obamacare: by driving up the cost of coverage and then doling out subsidies to some people and not to others, the law creates winners and losers.

As we move forward, haltingly, with full implementation, we shouldn’t forget about the losers. After all, as even Ezra Klein is now admitting, the entire Obamacare scheme depends on the young and healthy subsidizing coverage for everyone else by paying higher premiums. Maybe it’s time to start thinking about what will happen if they don’t.

Mr. Davidson is a writer based in Austin, Texas, and a health care policy analyst at the Texas Public Policy Foundation.