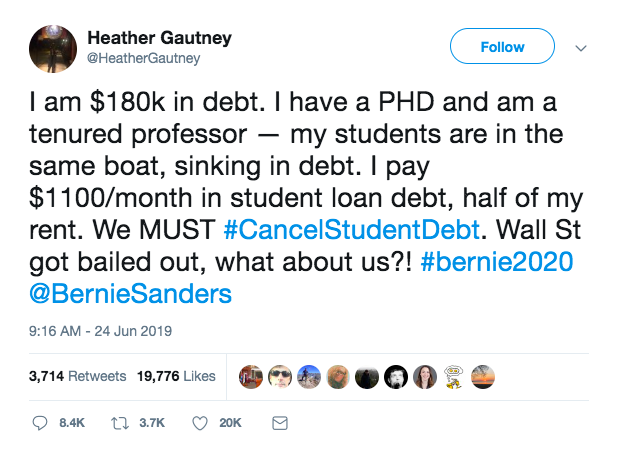

Yesterday, one of presidential contender Bernie Sanders’ campaign lackeys tweeted out what should surely be considered one of the worst ideas of this election cycle.

This idea, gaining traction under the hashtag #CancelStudentDebt following the release of Sanders’ college debt forgiveness plan, is bad for several reasons, but naturally appealing in a sort of populist way, since plenty of people choose not to think about second-order impacts and potential consequences of driving our country into even more ruinous national debt than before.

For starters, Gautney, per her Twitter profile, is an associate professor of sociology at Fordham University, a private school located in New York City. None of this is a problem on its own; in a free society, people should be able to tweet whatever dumb things they want while working in whichever industry or field of research.

However, according to publicly available data, associate professors at Fordham make an average of $111,700 per year. This excludes the value of their benefits, so final compensation is a good bit higher. It’s worth noting that the vast majority of professors at Fordham fall into the “associate professor” or “professor” category (full professors make, on average, $159,800 annually). So, 486 of Fordham professors fall into these well-paid and elite categories, while 224 fall into non-six-figures categories (assistant professor, instructor, and lecturer titles).

In other words, living in New York City and making a hefty wad of cash each year isn’t so oppressive, and the majority of Gautney’s colleagues are doing alright. That aside, Gautney consented to this field, job, and city, so if she has an issue with compensation or cost of living, switching to a more lucrative field or cheaper place to live is a decision she should make for herself, not a decision that ought to be bailed out by unsuspecting taxpayers who played no role in the choice.

"DoN't BoRrOw MoNeY yOu CaN't AfFoRd To PaY bAcK" says generation that spent years telling younger generations they absolutely needed a college degree to get a decent job with a side of subprime mortgages. #CancelStudentDebt

— Aaron Cynic (@aaroncynic) June 24, 2019

Sanders’ Grand Plan

Still, plenty of other people have greeted the Sanders plan with fanfare. If elected, Sanders would have taxpayers pay off the $1.6 trillion in student debt held by 45 million Americans. According to Washington Post, he’s “proposing to pay for the legislation with a new tax on financial transactions, including a 0.5 percent tax on stock transactions and a 0.1 percent tax on bonds,” which is a terrible idea in and of itself, as it would disincentivize investing.

What Bernie isn’t proposing to fix is the convergence of factors that lead to the high cost of college. Bailing people out instead of fixing deeper problems would be a foolish mistake. Colleges pump up their endowments and create bloated administrations, then expect students to grapple with enormous price tags.

But things don’t need to be like this: Mitch Daniels, president of Purdue University in Indiana, has frozen tuition at 2012 rates, so incoming freshmen in 2019 are locked into these cheaper prices. Currently, per Forbes, “In inflation-adjusted dollars, Purdue costs $4,000 less per year for out-of-state students than it did when [Daniels] took the job in 2013. In-staters pay nearly $3,000 less, at just under $23,000 this academic year for tuition, room, board and expenses.”

Daniels’ plan hasn’t been free of controversy, but it does make more sense than the current system:

In 2016 he introduced income-share agreements. Students who exhaust federal loans can fund their education with an agreement to sign over a share of their future income, usually between 3% and 5% for up to ten years after they graduate. (Repayments are capped at 2.5 times initial costs.) Critics hate ISAs because they’re unregulated and untested. Milton Friedman is said to have invented the idea but famously noted that they were ‘economically equivalent … to partial slavery.’ Daniels says, ‘If you want indentured servitude, it’s the student-loan program. With ISAs, the risk shifts entirely to the lender,’ since grads who don’t find work pay nothing.

Innovative practices aside, it’s up to consumers to exert pressure on colleges and hold them accountable for such wasteful, bordering on deceitful, practices. There’s no real reason why tuition costs must keep climbing.

Federal Spending Makes Student Costs Way Worse

We can’t pretend federally-subsidized loans don’t play a massive role. Even left-leaning outlets like Slate acknowledge this basic truth, drawing on data published in 2015 by the Federal Reserve Bank of New York and Brigham Young University:

Looking at both public and private nonprofit colleges during the mid-2000s, they found that schools raised tuition by 55 cents for each $1 increase in Pell grants their undergraduates received, and by 60 to 70 cents for each extra dollar of subsidized student loans.

Why would this happen? As the Roosevelt Institute’s Mike Konczal points out, the answer is a little less obvious than you might assume—in a world of rational econo-bots, people aren’t supposed to willingly pay more for an investment, such as a college degree, just because they can get a loan for it.* But the reality is that there are still lots of 18-year-olds who will pay more or less whatever it takes to attend the college of their choice so long as they can find the cash. By letting students borrow more, the government may just be inviting schools to raise tuition, knowing kids simply respond by taking on extra debt.

Still, even with the widespread availability of such subsidized loans, the college debt crisis isn’t necessarily as bad as many claim, which is sure to be unpopular to those who feel like their burden is unjust. Reason’s Nick Gillespie writes, “According to data from Lending Tree, for instance, about 70 percent of the class of 2018 took out loans; their median monthly payment was $222. The average loan amount (which will be higher than the median) for graduates with debt was about $30,000.”

The debt load for those who pursue law or medical school will undoubtedly be higher, and might be stacked on top of existing debt incurred by undergraduate degrees. Still, those who pursue careers in legal or medical fields can look forward to massive returns; in these circumstances, there’s no real need for debt to be forgiven since this is the cost of entry into an ultimately higher-paying field.

For those who pursue advanced degrees out of boredom or difficulty getting a job, with no clearly mapped-out ROI, that debt should also not be forgiven. It’s not taxpayers’ fault that someone spent a lot of money she doesn’t have without a clear vision for how that degree could improve her later financial prospects.

College Admissions Counselors Have Bad Incentives

Then there are the social and cultural factors to consider: we currently have a system where college admissions counselors for high school students have no real skin in the game. If anything, their incentives are completely misaligned, even diametrically opposed, to the incentives of the students they’re supposedly helping. We should push back on this completely idiotic system we’ve created.

Parents and admissions counselors need to recognize that a small dose of tough love now will pay dividends later on. No student should bank on populist election-year whims bailing him out. Instead, parents and college counselors ought to have frank conversations with the students they’re shepherding into adulthood about fiscal responsibility and how student loan payments will factor into these students’ monthly budgets later in life.

There’s also the practical financial component: canceling debt would take $1.6 trillion. The money for this program, and the many others being proposed by the likes of Sanders and Sen. Elizabeth Warren, cannot be gotten from taxing just, say, millionaires over a certain threshold—especially since we’re hitting up those millionaire purses for every other thing on the agenda.

You can’t spend the same money twice, although every single Democratic presidential contender seems to be fruitlessly trying. So in order to have this scale of college debt bailout, we would need to tax significant swaths of the population, including a good number of middle- and upper-middle class earners. This sends a very clear message: we care about making the loads of relatively well-off students with decent financial prospects a bit lighter instead of helping much poorer Americans with fewer prospects.

That Sanders’ proposal lacks any sort of means-testing requirement makes it clear that he believes this is something all people deserve, but it’s unclear why, or how that’s a worthwhile investment given that it will be allocated toward those who are relatively rich (or could have been relatively rich had they not gotten a useless master’s degree that doesn’t translate into higher earnings).

"If we #CancelStudentDebt everybody can afford to go to college!"

Umm… *You* wanted to go to college. Others balk at the idea of 4+ years studying topics that bore them. They prefer the trades and starting businesses.

Pay for your own preferences.

— J.D. Tuccille (@JD_Tuccille) June 25, 2019

Even if all these other points are uncompelling to some, there’s a bigger, broader lesson to be learned here: why are we inviting more intrusion of other people into our personal lives? I think Gautney’s professional choices are foolish; they’re different than the ones I would make. The only reason I’m mentioning that is because she’s asked me, or people richer than me, to pay for these choices. Had she not, I’d have nothing to say about her career decisions.

The less intrusion into our private choices, the better, both for personal freedom and for creating a cohesive society that doesn’t feel it’s appropriate to cast judgment on the lifestyles other people choose to live. Feeling like we have to pay for other people’s foolish choices just breeds resentment, whether that resentment is warranted or not. So, the cost of this proposal is even higher than the already-flabbergasting $1.6 trillion.